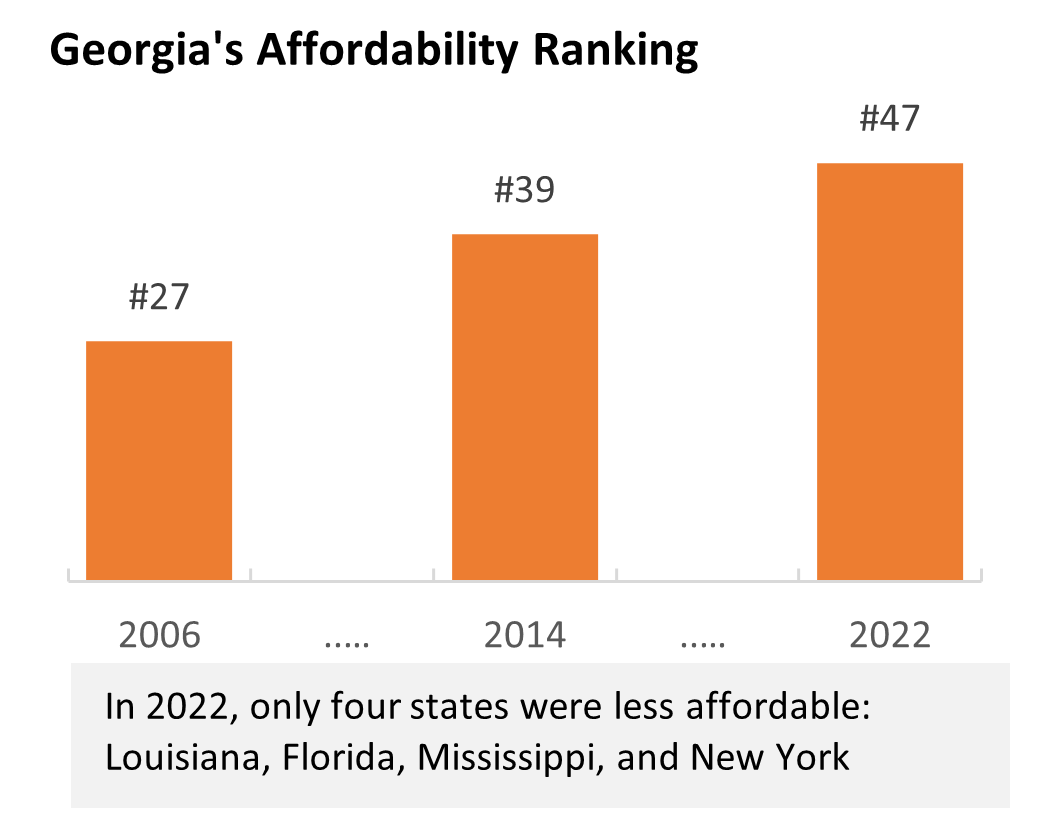

The affordability of personal auto insurance in Georgia has deteriorated in recent years, with the state climbing the ranks of least affordable states over the past decade and a half. In 2022, the most recent year for which expenditure data is available, personal auto insurance expenditures accounted for 2.0 percent of the median household income in Georgia, compared with the 1.5 percent share in the U.S. as a whole. Georgia ranked 47th in terms of auto insurance affordability, with only four states showing higher expenditure shares: Louisiana, Florida, Mississippi, and New York. This is a marked deterioration from Georgia’s past affordability position; in 2006, Georgia was the 27th most affordable state.

Affordability issues in Georgia’s auto insurance market stem from multiple factors. Many of them are the same as have faced the rest of the United States, such as economic inflation, high replacement costs, poor driving behavior, and legal system abuse. However, several key measures of cost drivers are higher in Georgia, including the propensity to file an injury claim once an accident occurs, underinsured motorists, and claim litigation.

Georgia’s auto insurance affordability ranking has been deteriorating for several years, with rising claim costs and concerns about increased litigation.

Litigation in auto insurance claims is a growing concern in Georgia, especially as tort reform in neighboring states is potentially pushing legal firms in those states to find opportunities elsewhere. Georgia has experienced elevated attorney advertising rates, particularly in television advertising. According to a report by the American Tort Reform Association (ATRA), more than $160 million was spent on more than 2.2 million local legal services advertisements in Georgia in 2023, an increase of nearly 40 percent since 2019, outpacing inflation. In addition, Georgia topped ATRA’s list of jurisdictions with problematic litigation environments for the second consecutive year in the 2023– 2024 report.

The affordability of homeowners insurance in Georgia, while not a focus of this report, is also a concern. Georgians spent 2.3 percent of household income on homeowners insurance in 2021, earning a ranking of 42nd on the list of affordable states for homeowners insurance. With aboveaverage exposure to natural weather risks, such as hurricanes, the state could risk an affordability crisis if litigation in homeowners claim becomes a significant issue. 1

Georgia’s Deteriorating Affordability

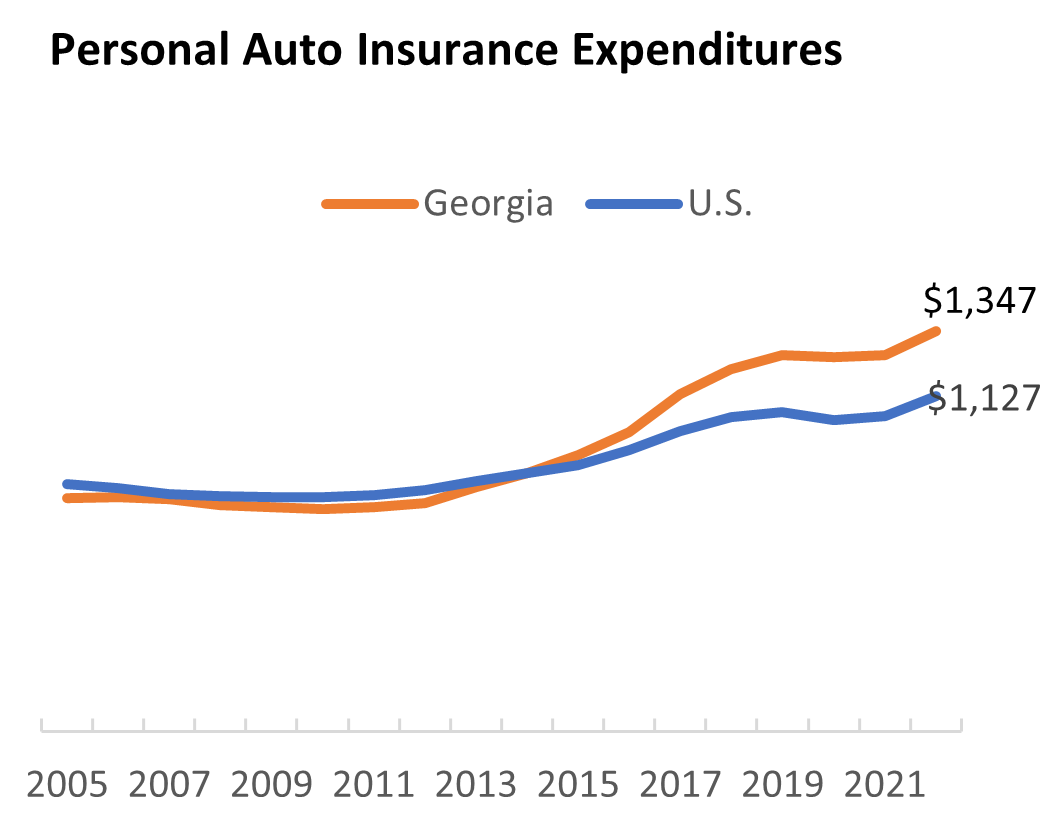

Georgia’s personal auto insurance spending, once very similar to the U.S. average, has accelerated in recent years. From the mid-2000s through 2014, Georgians spent about the same as other Americans to insure a vehicle. Starting in the mid-2010s, however, auto insurance expenditures in Georgia have escalated. Between 2014 and 2022, auto insurance spending in Georgia grew 5.6 percent annualized, compared with 3.3 percent in the country overall and faster than in any other state. In 2022, Georgia’s average expenditures of $1,347 were 20 percent higher than the U.S. average.

While auto insurance was becoming more expensive in Georgia relative to the U.S. average, income growth in the state was lagging. Between 2006 and 2014, median household income grew just 0.1 percent annualized in Georgia, among the lowest in the country. Income growth picked up between 2014 and 2022 but still lagged the U.S. rate. In 2022, median household income in Georgia was 9 percent lower than the U.S. average.

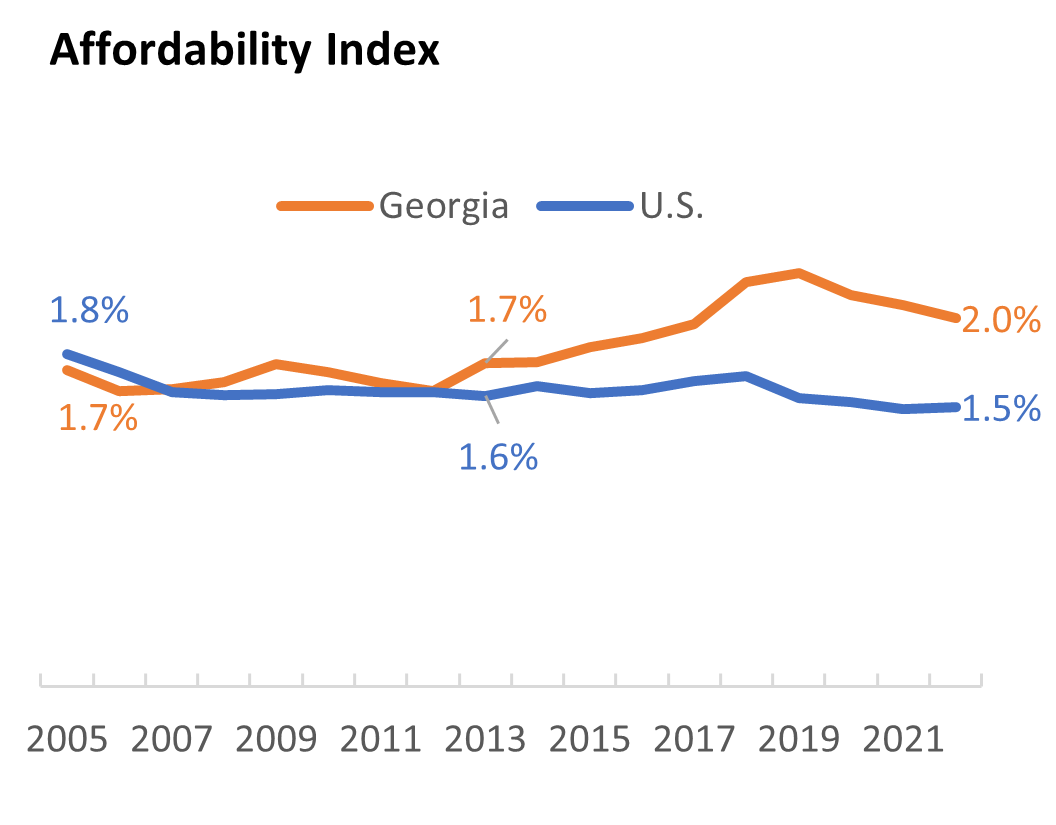

With below-average income and above-average expenditures, Georgia has become one of the least affordable states for personal auto insurance. In 2022, the ratio of average personal insurance expenditures to median household income was 2.0 percent in Georgia, up from 1.6 percent in 2006 and 1.8 percent in 2014. In contrast, the countrywide expenditure share fell from 1.7 percent in 2006 to 1.5 percent in 2022.

With this increase in Georgia’s personal auto expenditure share of income, the state’s affordability ranking has deteriorated from 27th most affordable state in 2006 to the 47th most affordable state in 2022. Only four states— Louisiana, Florida, Mississippi, and New York— were higher in 2022.

Auto Insurance Cost Drivers: How Georgia Compares

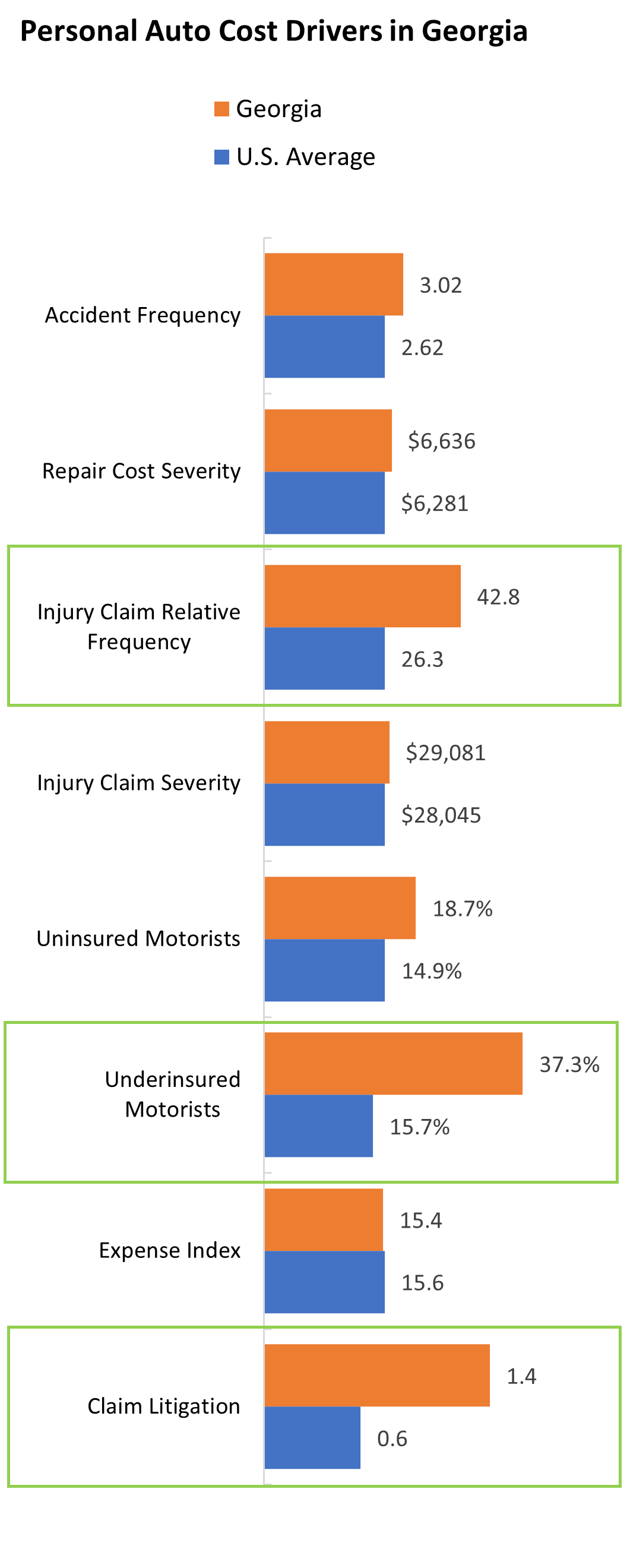

Insurance affordability is determined by the underlying key cost drivers, which must be addressed to improve affordability. IRC compiled several factors that contribute to rising costs not only in Georgia, but also across the country. Georgia results are well above the national average in injury claim relative frequency and claim litigation. 2

Accident frequency: The number of property damage liability claims per 100 insured vehicles in Georgia is 15 percent higher than the U.S. average.

Repair cost severity: Average repair costs in Georgia are slightly higher than U.S. average.

Injury claim relative frequency: Georgians show a greater propensity to file injury claims once an accident has occurred, with a relative bodily injury (BI) claim frequency 60 percent higher than the U.S. average.

Injury claim severity: The average amount paid for bodily injury insurance claims in Georgia is slightly higher than the U.S. average.

Uninsured motorists: The uninsured (UM) rate in Georgia is 25 percent higher than the U.S. average.

Underinsured motorists: Georgia has one of the highest rates of underinsured (UIM) motorists in the country, more than twice the U.S. average.

Expense index: The costs associated with claim settlement are similar in Georgia as in the country as a whole, as measured by the amount insurers spent to process, investigate, and litigate claims (loss adjustment expenses) as a percentage of incurred losses.

Claim litigation: The rate of litigation in personal auto claims in Georgia is more than twice the rate in the median state.

Recent Movement in Key Cost Drivers

The combined average loss cost, which measures the dollars paid under both bodily injury and personal injury protection coverages averaged over all insured vehicles, including those without accidents, provides a way to compare injury claim losses across states. A decade ago, the average injury loss cost in Georgia was $158, slightly below the U.S. average. Injury costs grew steadily through 2019, with Georgia outpacing the countrywide average, before falling everywhere in 2020 with the start of the pandemic. Since 2020, Georgia has shown the highest growth rate in the country, nearly double the countrywide rate. In 2023, the average injury cost per insured vehicle was $376 in Georgia, almost 60 percent higher than the $237 in the U.S. overall.

Litigation in Georgia auto claims is a growing concern. According to one measure, the rate of private passenger litigation in the states is nearly three times that in the median state. This litigation measure is considerably higher in Florida (5.0) and Louisiana (2.3); tort reform efforts in those nearby states may cause attorneys to seek more lucrative litigation environments and result in increased legal activity in Georgia.

Uninsured and underinsured motorists are both a symptom and a cause of affordability issues. When affordability deteriorates, whether from increasing costs or slower income growth, increasing numbers of motorists may choose to lower the policy limits or to forgo the mandated insurance completely. The resulting need for drivers to purchase UM and UIM protection further increases average expenditures on insurance. Both the UM and UIM rates are higher than average in Georgia. The UIM rate is especially high in the state: Georgia’s UIM rate has been increasing steadily and was the third highest rate in the country in 2022.

Notes

- See IRC’s 2023 report Homeowners Insurance Affordability: Countrywide Trends and State Comparisons.

- For more information about how these cost drivers are defined, see IRC’s 2022 report State Variations in Auto Insurance Affordability or 2021 research brief Auto insurance Affordability: Countrywide Trends and State Comparisons.

- Accident frequency is 2022 data from the IRC study Trends in Personal Auto Insurance Claims: 2002–2022.

- Repair costs reflects property damage liability claim as described in the IRC study Trends in Personal Auto Insurance Claims: 2002–2022, updated for 2023 data.

- Injury claim relative frequency is the number of bodily injury claims for every 100 property damage liability claims, as described in the IRC study Trends in Personal Auto Insurance Claims: 2002–2022, updated for 2023 data.

- Injury claim severity is the mean payment for bodily injury claims, as described in the IRC study Trends in Personal Auto Insurance Claims: 2002–2022, updated for 2023 data.

- Uninsured motorists rate is the ratio of uninsured motorists claim frequency to bodily injury claim frequency in 2022, from IRC’s report Uninsured Motorists, 2017–2022.

- Underinsured motorists rate is the ratio of underinsured motorists claim frequency to bodily injury claim frequency in 2022, from IRC’s report Underinsured Motorists, 2017–2022.

- Expense index reflects loss adjustment expenses as a percentage of incurred losses, 2017–2022 average, based on data from NAIC’s Report on Profitability by Line by State.

- Claim litigation reflects the percentage of personal auto claims with litigation, based on data from NAIC's Market Conduct Annual Statement Scorecard and measured by the ratio of suits opened to claims closed without payment multiplied by the ratio of claims closed without payment to the total claims closed.